Palantir - the Next Frontier?

Price Targets - Base Case: $21 | Bull Case: $70

Palantir stock is up over 3x since its IPO a few months ago. Given the impending earnings announcement, I thought it would be interesting to analyze the company to determine if the stock is worth buying.

TLDR – it’s anyone’s guess how Palantir’s business will evolve over the next decade. The stock has the potential to double from here, so it may be worth having a small position.

Business

Palantir is in the business of selling software to large institutions – governments and corporations.

They currently have two platforms – Gotham and Foundry. Gotham enable users to identify patterns hidden in data and was used by US defense and intelligence agencies in Afghanistan and Iraq. Foundry “transforms the ways in which organizations interact with information by creating a central operating system for their data.”

Palantir estimates its TAM to be $119B across commercial and government. Given the company has been around since 2003, and will only break $1B in revenue in 2020, it’s unclear how much of this TAM it will actually be able to capture. The market is obviously massively bullish on the company at the moment, and by my calculations, Palantir would need to be doing about $20B in revenue in 2030 with 15% operating margins to justify today’s price. While this is certainly possible, things need to go very well for Palantir over the next decade.

Valuation

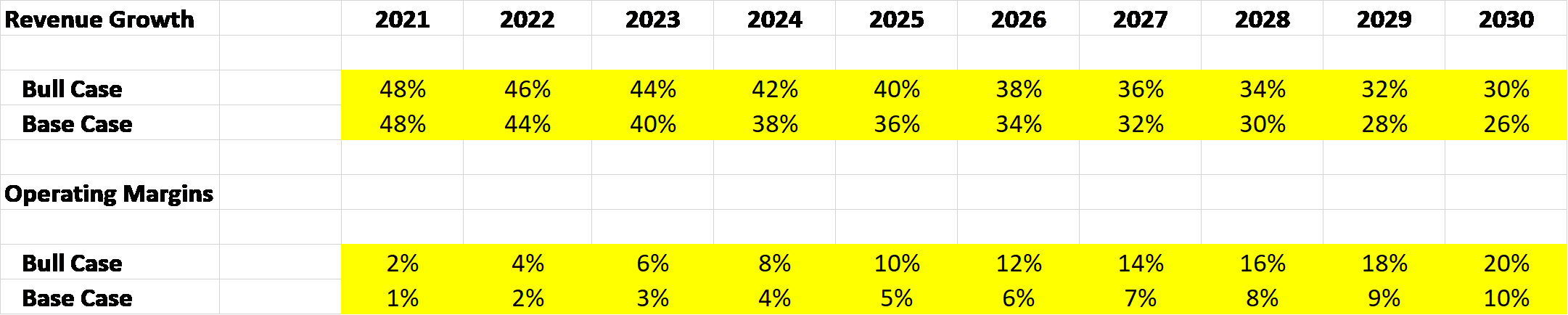

I look at two scenarios with Palantir – a base case and a bull case.

Below are revenue growth and operating margin assumptions for each of these cases.

As you can see, even the base case assumes very strong revenue growth over the next decade with operating margins slowly improving by 1% each year. To me, this is an optimistic, but plausible outcome for the company over the next decade.

The bull case assumes Palantir is at an inflection point and is about to grow massively ($30B in revenue by 2030) and profitably. The story here could be that a much larger percentage of the $1T military budget will be spent on software going forward, and that Palantir will be the primary beneficiary.

I assume a terminal value multiplier of 25x FCF for the base case and 35x FCF in the bull case. Based on these assumptions, I arrive at a per share value of $21 in the base case and $70 in the bull case.

As always, my model is available here if you’d like to use your own assumptions.

Portfolio Allocation

Given the inherent uncertainty with the company, I’d prefer not to buy the stock above $20. However, at the same time, I recognize that this could be “the next Salesforce” and we’re in a market where stories prevail over numbers. Tesla anyone? Therefore, my strategy is to buy a small position in the stock and to also sell Jan 2022 $65 calls for $7 each. While this caps my upside to ~100%, it feels like a good trade given my base case is already relatively bullish and the stock could easily fall to $20. The calls effectively hedge a 20% loss on the stock position.

Risks

About 60% of Palantir’s revenue is currently from governments and if the U.S. government decides Palantir is not a company that they want to partner with, it would be devastating for the business.

Palantir spent $450mm on sales and marketing in 2019 vs $306mm on R&D. For a company that supposedly has incredible software, this is a little surprising and may be a red flag. I understand the lifetime value of customers is high, so the strategy may be to spend whatever it takes to bring customers onto the platform, but this could also mean Palantir’s products are not as differentiated as the company would like you to believe and therefore competition will be strong over the next decade.

Fantastic write up as usual. I think you're on to something when you compare the sales/marketing spend to the R&D spend. I never thought of that. Good catch.