Versant

Maybe a Few Puffs in the Cigar Butt

Versant was spun off from Comcast in early 2026 and now trades on the NASDAQ under ticker VSNT.

Like a lot of spinoff’s, the stock has been crushed out of the gate as some holders of Comcast are forced sellers. See chart below –

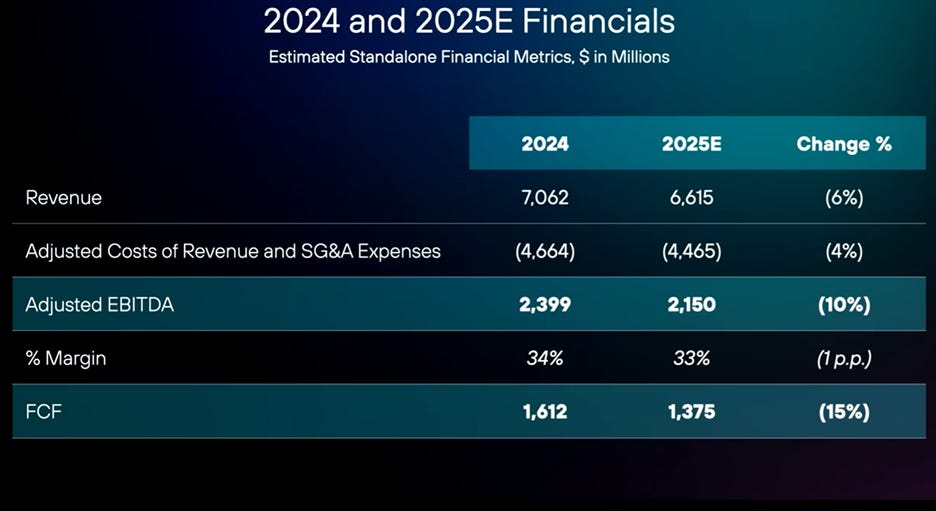

The story here is not exactly compelling. Versant is a collection of ‘legacy media’ businesses and 80% of their revenue comes from linear TV, which is a dying business. See financial snap shot below from the December 2025 investor day.

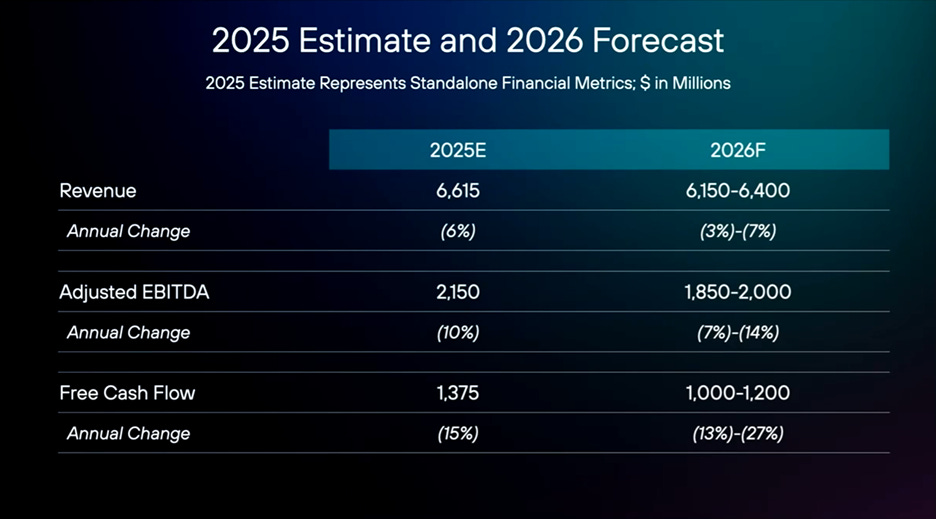

The guidance for 2026 is not going to get anyone excited either - snapshot below.

Free cash flow (FCF) potentially shrinking 25% is not something investors get excited about.

Based on the commentary from the investor day, my sense is that management is going to try and slow FCF shrinkage by focusing on costs, so I expect it to decline by about 10% a year for the next 10 years. In this scenario, starting at 1.1B in FCF in 2026, the cumulative 10 year FCF generated by the business would be about $7B. I’ve found that paying 10x average forward FCF is generally a decent bet, so with the market cap at $4.7B today, this could be an attractive set up.

The company has $2.3B in net debt, so from an EV stand point its exactly at 10x average forward FCF.

If you bought the business in its entirety today, you could use the FCF to pay yourself back over the next five years, recouping your cost, and then whatever it’s spitting out would be gravy. Given it’s likely doing 500m in FCF in five years, it’s effectively a 10% go forward yield on the equity. As I write this, I realize it’s not that compelling, but you do get all your capital back in five years, so the downside is low.

What could go well?

FCF stabilizes at about $750m (a 15% margin on $5B in steady state revenue). They accomplish this by better monetizing unique assets like CNBC and keeping costs under control.

We could reach a steady state in linear TV watchers in the country, so the decline in revenue slows to low single digits. Maybe the most eager cord cutters have already left.

What could go wrong?

The Citrini unemployment scenario plays out and linear TV subscribers decline faster than expected. This is going to be very difficult for Versant to overcome if it plays out. Unlike the market, I ascribe a 50% probability to unemployment reaching 10% in the next three years, so the risk here is very real. The offset is that its likely mostly older retired Americans watching linear TV, so maybe white collar job loss doesn’t actually hit VSNT that hard.

FCF falls faster than 10% a year as management invests FCF into businesses with poor long term prospects instead of returning cash to shareholders. Because the spin is so new, management effectively has no track record of capital allocation to evaluate.

Even if TV subscribers hold up, advertising spending on linear TV could continue to shrink as advertisers channel spending to the platforms with the best ROI – think Meta. This likely results in lower revenue for the Versant’s linear channels and is the single biggest headwind to this business over the next ten years.

Given the puts and takes, I can justify holding only a very small position (~1%) in my portfolio. If the stock pops 30% or more at any point over the next year, I will take my profits and move on.